DRDGOLD LTD-SPONSORED ADR (NYSE:DRD) Identified as a Peter Lynch-Style GARP Investment

Investors looking for long-term growth opportunities at reasonable prices often consider strategies that combine fundamental strength with sustainable expansion. One such method is the approach made famous by well-known investor Peter Lynch, which centers on finding companies with strong earnings growth, good financial health, and appealing valuations. This method, often grouped as Growth at a Reasonable Price (GARP), steers clear of speculative investments in favor of businesses that show consistent, manageable expansion. The filtering process focuses on important measures like earnings growth, return on equity, and debt levels to find companies able to provide continued performance. A recent filter based on these ideas has identified DRDGOLD LTD-SPONSORED ADR (NYSE:DRD) as a possible candidate deserving of more examination for investors who agree with this point of view.

Alignment with Peter Lynch Criteria

DRDGOLD seems to fit well with several main parts of the Peter Lynch investment method. The filter specifically looks for companies showing solid but sustainable growth, fair valuation when considering that growth, and a good financial base. DRDGOLD’s fundamental measures meet these requirements, placing it as a company that has expanded successfully without taking on too much financial risk.

- Earnings Per Share Growth: The company reports a five-year average EPS growth of 26.15%. This number falls within the Lynch filter’s goal range of 15% to 30%, pointing to a record of solid, yet potentially sustainable, profit increase that is not too fast to be unstable.

- Valuation Compensated for Growth: An important Lynch measure is the PEG ratio, which compares the Price-to-Earnings (P/E) ratio to the earnings growth rate. DRDGOLD’s PEG ratio of 0.46 is well under the filter’s limit of 1. This indicates the stock is trading at a price that may not completely match its past growth, a main signal of a fair price for a growth investor.

- Strong Profitability and Financial Health: The company shows very good profitability with a Return on Equity (ROE) of 36.17%, much higher than the 15% minimum needed by the filter. Also, its Debt-to-Equity ratio is almost zero at 0.001, showing very little use of debt financing—a sign of financial steadiness that Lynch preferred. The Current Ratio of 2.28 also supports the company’s ability to easily meet its short-term responsibilities.

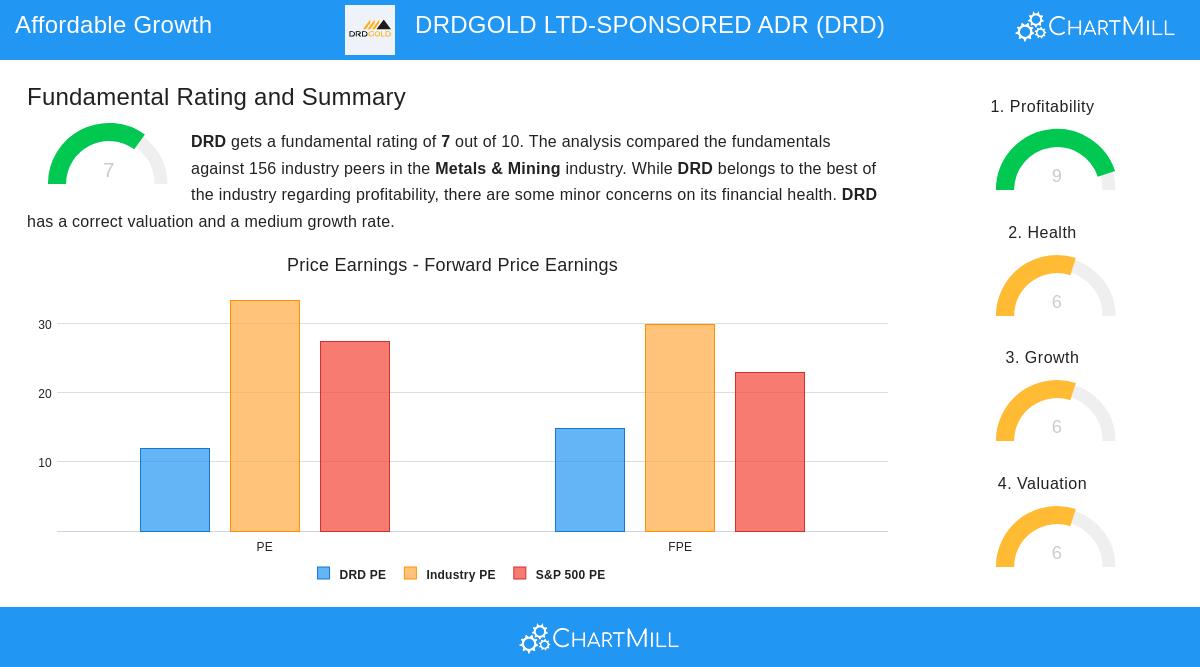

Fundamental Analysis Overview

A closer look into DRDGOLD’s fundamental profile supports the initial filtering outcomes. The company gets an overall fundamental rating of 7 out of 10, suggesting a good position within the Metals & Mining industry. Its biggest advantage is in its profitability, where it gets a 9 out of 10. Important margins, including Profit, Operating, and Gross Margin, are not just high but have gotten better in recent years, and its Return on Invested Capital (ROIC) is very good.

The company’s financial health is also strong, scoring a 6 out of 10, with specific advantage in solvency because of its very low debt. From a valuation point of view, with a score of 6, DRDGOLD’s P/E ratio of 11.96 is seen as inexpensive compared to both its industry competitors and the wider S&P 500 index. While its growth score is a moderate 6, it is significant to see that this shows a change from very high past growth to more measured, and possibly more sustainable, predicted future growth. For a detailed look at these measures, you can examine the full fundamental analysis report.

Business Model and Context

DRDGOLD’s business model, which centers on the retreatment of surface gold tailings in South Africa, matches with Lynch’s concept of investing in understandable, if not especially “glamorous,” businesses. The company works in a particular area, creating value by reprocessing old mining waste. This operational focus has produced the solid financial measures noted above. While the company’s dividend yield of 1.72% is not a main point for growth investors, its payout ratio is sustainable, and it has a long history of payments.

Conclusion and Further Research

Based on a quantitative filter built from Peter Lynch’s ideas, DRDGOLD presents an interesting profile for investors looking for growth at a reasonable price. It shows a strong mix of high profitability, a very clean balance sheet, a history of solid earnings growth, and a valuation that seems modest. The company’s simple business model in gold retreatment increases its attractiveness for those who prefer understandable businesses.

It is significant to note that a filter is a beginning for research, not a final suggestion. Potential investors should do more investigation on elements like the geopolitical environment of its operations, future gold price outlook, and the progress of its growth strategies.

This examination of DRDGOLD was found using a stock filter based on the Peter Lynch method. If you are curious about finding other companies that meet these requirements, you can view the complete filter results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy, sell, or hold any security, or an endorsement of any investment strategy. All investments involve risk, including the possible loss of principal. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions.