Toll Brothers Inc (NYSE:TOL) Screens as a Peter Lynch-Style GARP Investment

The investment philosophy created by Peter Lynch, described in his book One Up on Wall Street, focuses on finding companies with good growth prospects that are trading at sensible prices. This “Growth at a Reasonable Price” (GARP) method steers clear of the extremes of pure growth or deep value investing. Instead, it looks for businesses showing consistent earnings expansion, good financial health, and profitability, all while making sure the stock’s price has not exceeded its growth potential. The method depends on fundamental analysis and a long-term buy-and-hold perspective, stressing the importance of investing in companies that are easy to understand and have lasting competitive advantages.

TOLL BROTHERS INC (NYSE:TOL) appears as a candidate from a screen constructed on Lynch’s ideas. The luxury homebuilder works in a sector that, while cyclical, is fundamentally easy to grasp, people will always need housing. The company’s concentration on the luxury segment and its integrated business model, which contains its own financing and manufacturing operations, gives a degree of control over its activities.

Meeting the Lynch Criteria

A main part of Lynch’s method is finding companies with good, but not extreme, earnings growth. He preferred annual EPS growth between 15% and 30%, thinking growth above that rate is frequently not maintainable. Toll Brothers shows a strong track record here, with a five-year EPS growth rate of about 28.0%. This puts the company directly within Lynch’s desired range, pointing to a good yet possibly maintainable growth path.

To make sure investors are not paying too much for that growth, Lynch used the PEG ratio (Price/Earnings to Growth). A PEG ratio of 1 or lower implies the stock may be sensibly valued compared to its growth rate. Toll Brothers does well in this area, having a PEG ratio of only 0.35. This low number implies the market may be setting a low value on the company’s past earnings growth.

Lynch also emphasized financial health to avoid companies at risk during economic slowdowns. The screening criteria contain checks for low debt and enough cash.

- Debt-to-Equity Ratio: Toll Brothers reports a ratio of 0.35, which is not just below the screen’s limit of 0.6 but also nears Lynch’s more strict preference for a ratio below 0.25. This points to a careful capital structure with less dependence on debt financing.

- Current Ratio: The company’s current ratio of 3.54 is much higher than the needed minimum of 1, indicating a good capacity to meet its immediate debts.

Finally, profitability is measured by Return on Equity (ROE). Lynch searched for companies producing an ROE above 15%, a mark of efficiency in using shareholder money. Toll Brothers meets this need with an ROE of 17.36%, showing its ability to turn equity into profits well.

Fundamental Health Overview

A wider fundamental analysis of Toll Brothers supports the results from the Lynch-based screen. The company gets a good overall score, with specific good points in profitability. Its profit and operating margins are some of the highest in the household durables industry, showing efficient operations and pricing strength in its luxury market. Financially, the company is mostly healthy with a manageable debt level and a good current ratio, though it is important to see a lower quick ratio implies a large part of its immediate assets is in inventory, a typical feature for a homebuilder.

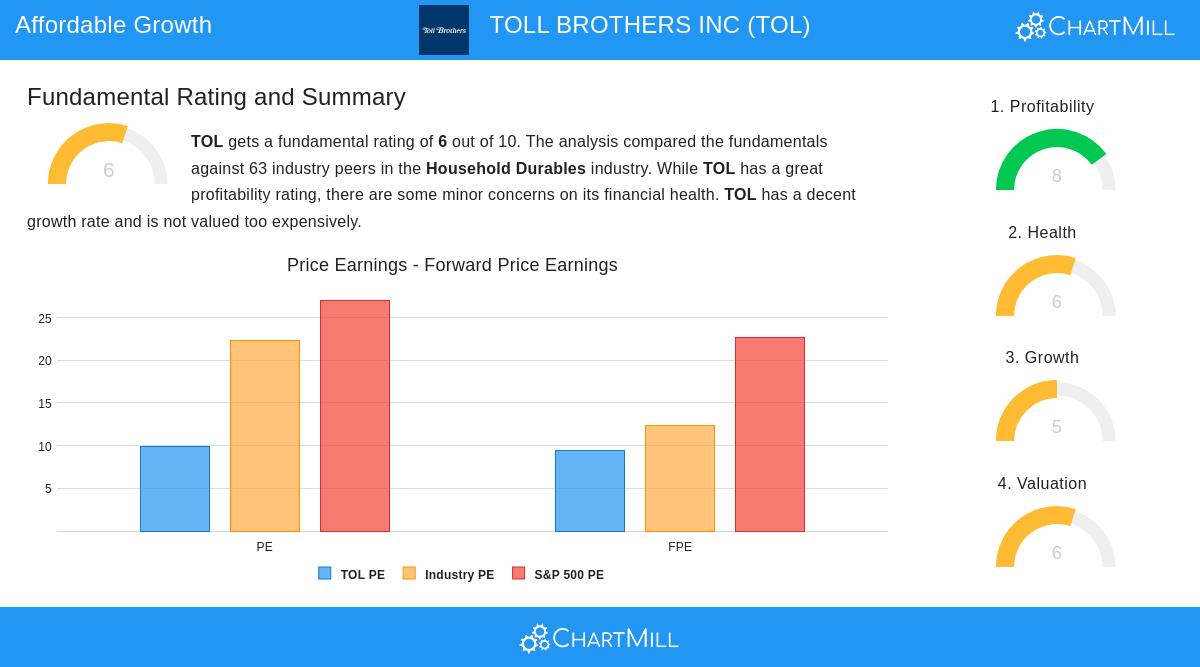

From a valuation viewpoint, the stock seems sensibly priced, trading at a P/E ratio below both the industry and S&P 500 averages. The primary area for attention is growth; while the historical 5-year growth is good, analyst forecasts predict a slowing in EPS growth to a still-sound high-single-digit percentage in the next few years.

A Candidate for Long-Term Consideration

For investors who follow Peter Lynch’s approach, Toll Brothers offers a strong case. It meets the quantitative filters made to find sensibly priced growth companies with good finances. The company works in a known industry and has shown a capacity to grow earnings at a maintainable rate while keeping high profitability. The current valuation measures imply the market may not be completely valuing this mix of growth and financial control. As with all investments, this screen acts as a beginning point for more detailed investigation into the company’s competitive environment, management, and future growth catalysts.

The Peter Lynch strategy screen can be a useful instrument for discovering possible long-term investments. You can find more companies that currently meet this screen by visiting the Peter Lynch Strategy Stock Screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.