OneSpan Inc (NASDAQ:OSPN) Emerges as a Peter Lynch-Style Investment Candidate

OneSpan Inc (NASDAQ:OSPN) has appeared as a candidate from a screening process based on Peter Lynch’s investment philosophy. This method focuses on finding companies with lasting earnings growth, fair valuations, and sound financial health, characteristics that match what Lynch called “growth at a reasonable price” during his time managing the Magellan Fund. The strategy stresses fundamental analysis instead of market timing, looking for businesses that can provide steady results over long periods rather than pursuing fast but unstable increases.

Investment Philosophy Foundation

Peter Lynch’s method focuses on finding companies increasing at a maintainable speed, typically between 15-30% each year, while keeping financial control. This method avoids both slow-moving businesses and very fast-growing companies where unstable growth often results in price swings. Lynch stressed investing in understandable businesses with solid competitive positions, acceptable debt levels, and good valuations compared to their growth potential. The strategy needs patience, as Lynch thought short-term price changes are hard to predict, but well-chosen companies tend to benefit investors over 10-20 year timeframes.

Growth and Valuation Alignment

OneSpan shows several features that match Lynch’s growth and valuation measures:

- Earnings Growth: The company has reached a 5-year EPS growth rate of 19.39%, placing within Lynch’s favored 15-30% maintainable growth band

- PEG Ratio: With a PEG ratio of 0.59 based on past earnings growth, the stock trades under Lynch’s limit of 1, suggesting the price may not completely account for growth potential

- Profitability Metrics: A return on equity of 24.70% greatly passes Lynch’s 15% minimum need, showing efficient use of shareholder money

These measures are important in Lynch’s framework because they find companies growing at a controllable speed while staying fairly priced. The PEG ratio especially helps prevent paying too much for growth, while strong ROE shows management’s skill in creating profits from equity.

Financial Health and Stability

Lynch put notable focus on financial strength to handle economic cycles and prevent too much risk:

- Debt Management: OneSpan holds no debt, greatly passing Lynch’s liking for debt-to-equity under 0.6 and his personal liking for ratios below 0.25

- Liquidity Position: The current ratio of 1.77 shows enough short-term cash, easily above Lynch’s 1.0 limit

- Cash Flow: Positive operating cash flow in the last year matches Lynch’s focus on real cash creation rather than only accounting profits

These financial health signs are basic to Lynch’s strategy because they lower bankruptcy danger and give companies room to invest during economic slumps without needing outside money.

Fundamental Assessment Overview

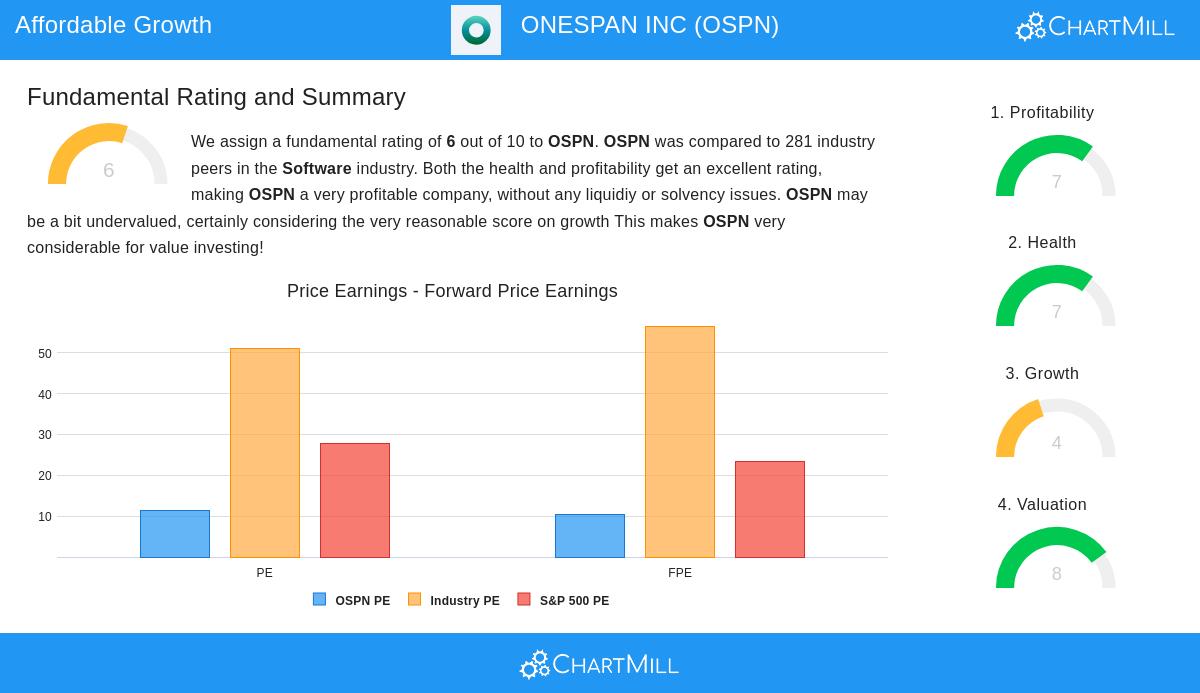

OneSpan’s full fundamental analysis shows a company with different strengths across various areas. The stock rates very well on valuation and profitability measures, with price-to-earnings ratios much lower than both industry and S&P 500 averages. Profitability numbers including return on assets (16.78%), return on invested capital (15.84%), and different margin measures all place in the top group compared to software industry peers.

The company’s financial health seems firm, especially because of the total lack of debt and good solvency measures. However, growth shows a varied image, while past EPS growth has been strong, income has decreased a bit over recent years, though analysts expect a return to small income growth in the future. For a detailed look at these fundamental parts, see the complete fundamental analysis report.

Strategic Considerations

For investors using a GARP method inspired by Lynch’s ideas, OneSpan offers an interesting case of a company with strong past profitability and good valuation trading at a price below its growth possibility. The company’s focus on digital security solutions meets a rising market need as transactions more often happen online, placing it in what Lynch might call a “dull but necessary” field instead of a risky technology wave.

The lack of debt gives important financial steadiness, while the fair valuation multiples provide a safety buffer. However, investors should note the recent income difficulties and watch if the company can get back to steady top-line growth while keeping its notable profitability numbers.

Exploring Additional Opportunities

For investors interested in finding other companies that meet Peter Lynch’s investment rules, more screening results can be found using the Peter Lynch Strategy Stock Screener. This tool allows more adjustment and finding of companies showing similar features of maintainable growth, financial health, and fair valuation.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions. Past performance does not guarantee future results.