Hormel Foods Corp (NYSE:HRL): A Dividend Stock Analysis for Income Investors

Investors looking for dependable income often consider dividend stocks, but finding companies that provide good yields and lasting payouts needs detailed study. One organized method uses filters for firms with good dividend traits while keeping enough profit and financial strength. This process helps remove companies with dividends that may not hold up, which could be vulnerable in economic declines. By concentrating on these basic supports, investors can create a collection of dividend stocks that supply income and a degree of safety in different market environments.

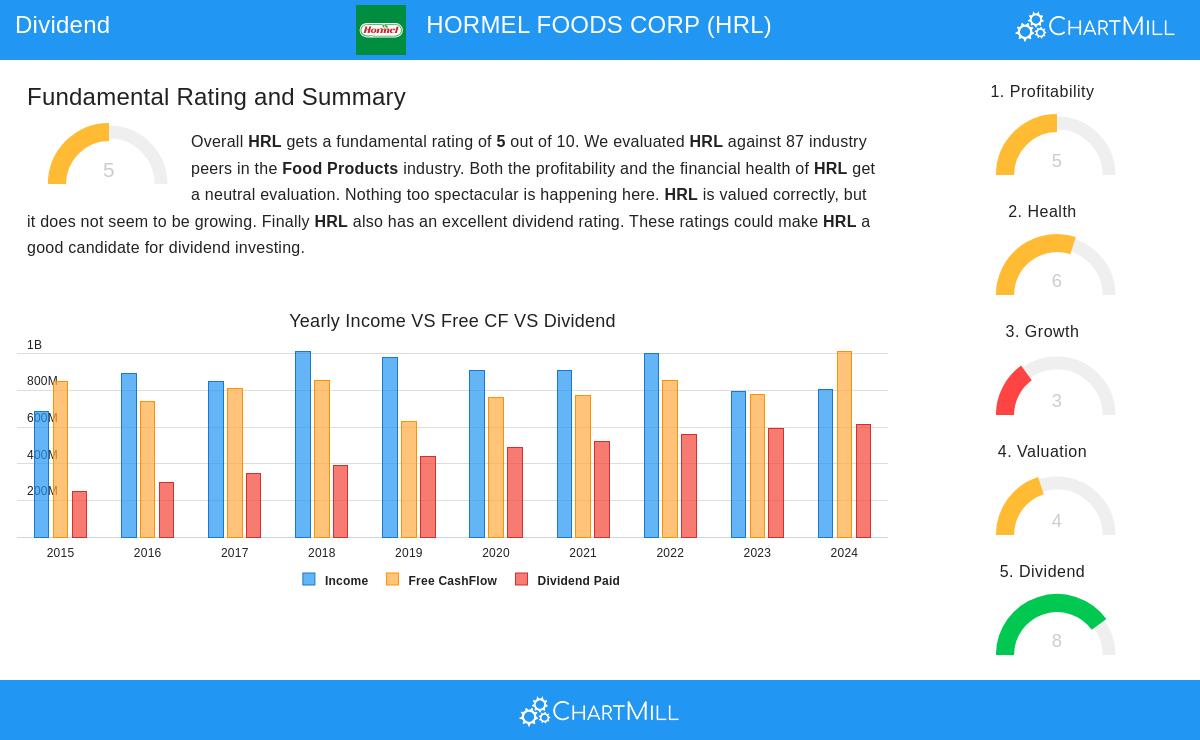

Dividend Strength and Lasting Quality

Hormel Foods Corp (NYSE:HRL) displays several notable traits for investors focused on dividends. The company’s dividend details indicate good present income and a background of steady payments, which are important for investors needing regular dividend income. The company holds a 4.70% dividend yield that is much higher than the S&P 500 average of 2.44%, giving investors income above the market norm. Also, Hormel has built a history of dividend dependability, paying dividends for at least ten straight years without cuts, showing dedication to shareholder returns even in tough economic times.

The dividend increase narrative further supports the investment view. Hormel has reached a yearly dividend growth rate of 6.53% in recent years, showing management’s belief in the company’s capacity to produce more cash flow. This steady growth pattern fits well with dividend investment plans that value not only present income but also defense against inflation via rising payments. Still, investors should see that the present payout ratio is 83.32% of earnings, which brings up some questions about lasting quality and needs watching in coming periods.

Profit and Business Results

Hormel’s profit measures, while not outstanding, give enough base to back its dividend payments. The company reaches a return on equity of 9.33% and return on assets of 5.59%, putting it in the high groups of its industry counterparts. These results show good use of shareholder money and assets to create earnings, which is needed to keep dividend payments without hurting financial soundness. The profit margin of 6.26% and operating margin of 8.40% also do better than most rivals in the food products field.

Even with these good total numbers, investors should know about some worrying directions in profit measures. Both profit margins and operating margins have shown drops in recent times, which might strain future dividend growth if not turned around. The company’s gross margin of 16.36% matches industry standards but has also faced downward push. These margin directions show the need for continued tracking, though present profit levels stay enough to support the current dividend plan.

Financial Condition Review

The company’s financial condition gives extra assurance for dividend lasting quality. Hormel keeps a solid current ratio of 2.47, showing enough cash to meet near-term duties, which is key for making sure dividend payments are made on time. The debt-to-equity ratio of 0.35 shows a careful capital setup with balanced use of borrowing, lowering money risk in economic slumps. The Altman-Z score of 3.62 points to low bankruptcy risk and places the company well in its industry.

From a solvency view, the debt-to-free-cash-flow ratio of 4.55 shows a middle stance, meaning that while the company has some debt, it stays within controllable levels compared to its cash creation abilities. The bettering debt-to-assets ratio versus earlier years shows active balance sheet care. These condition measures together support the dividend investment idea by showing the company’s ability to maintain payments through various economic phases without risking financial steadiness.

Value and Increase Factors

Hormel’s value shows a blended image for dividend investors. The company trades at a price-to-earnings ratio of 16.76, which is under the S&P 500 average of 27.86 and is more appealing than many industry peers. The forward P/E ratio of 15.78 also hints at fair value relative to future earnings forecasts. These value measures suggest investors are not paying too much for the company’s dividend income, giving some room for error.

Increase outlooks, however, stay moderate. Revenue has increased at 4.65% each year in recent years, with guesses for about 2.28% growth going forward. Earnings per share have dipped a bit in the past year but are expected to improve with 4.18% yearly growth ahead. While these increase rates may not thrill growth investors, they give enough base for ongoing dividend rises, which matches the goals of income-focused investors who value steadiness over fast growth.

For investors wanting to look at similar dividend chances, more filter results are available using the Best Dividend Stocks screener, which uses like standards for dividend quality, profit, and financial condition.

Disclaimer: This study is based on basic data and filter methods for information only. It is not investment guidance, and investors should do their own study and think about their personal money situation before making investment choices. Past results do not ensure future outcomes, and dividend payments depend on company choice and market factors.