Lantheus Holdings Inc (NASDAQ:LNTH) Presents a Compelling Value Investment Case

Lantheus Holdings Inc (NASDAQ:LNTH) has appeared as an interesting candidate through a methodical screening process made to find companies trading at appealing valuations while keeping good fundamental characteristics. This method specifically looks for stocks with good valuation metrics together with acceptable profitability, financial health, and growth potential,key criteria that match value investing principles. The process focuses on finding companies where the market price seems separate from basic business strength, possibly giving investors a chance to obtain quality assets at sensible prices.

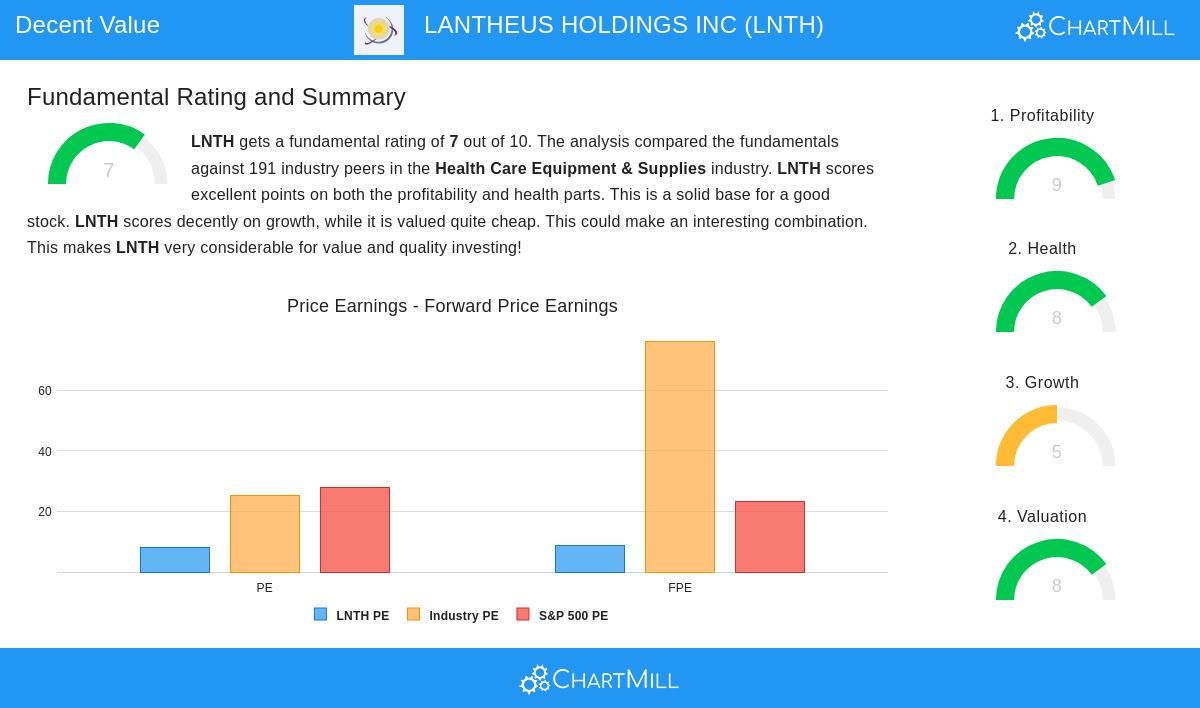

Valuation Metrics

The company’s valuation profile is noticeable as especially interesting, with several indicators hinting the stock may be trading below its intrinsic value. The fundamental review shows a few main valuation benefits:

- Price-to-Earnings ratio of 8.11, much lower than the industry average of 25.32 and the S&P 500 average of 27.76

- Forward P/E ratio of 8.66, less expensive than 95.81% of industry peers

- Enterprise Value to EBITDA ratio placing the company as more economical than 96.34% of competitors

- Price-to-Free Cash Flow ratio ranking better than 97.91% of industry counterparts

These valuation metrics are important for value investors looking for companies trading at discounts to their actual worth. The large discounts to both industry and broader market multiples indicate possible undervaluation, especially when viewed next to the company’s operational positives.

Financial Health Assessment

Lantheus shows sound financial health with a total rating of 8 out of 10, signaling a good balance sheet foundation. The company’s solvency and liquidity metrics give assurance in its capacity to handle economic variations:

- Current Ratio of 4.29 and Quick Ratio of 4.07, both much higher than industry averages

- Debt-to-Free Cash Flow ratio of 1.19, showing the company could pay back all debt in about 1.19 years

- Altman-Z score of 4.54, well inside the safe area and superior to 78.01% of industry peers

- Manageable Debt-to-Equity ratio of 0.49, consistent with industry norms

For value investors, good financial health lowers bankruptcy risk and allows operational flexibility. The company’s capacity to produce significant cash flow relative to its debt responsibilities builds a margin of safety,a central idea in value investing that guards against calculation mistakes in intrinsic value estimates.

Profitability Analysis

The company performs well in profitability with a high rating of 9 out of 10, hinting at efficient operations and good competitive standing. Main profitability metrics show operational quality:

- Return on Invested Capital of 18.03%, beating 96.86% of industry competitors

- Operating Margin of 28.64%, putting it in the top 4.19% of the industry

- Profit Margin of 17.82%, better than 93.19% of peers

- Steady betterment in margins across gross, operating, and profit measures over recent years

High profitability is vital for value investments because it signals lasting competitive benefits and the ability to create returns above the cost of capital. The company’s better returns on capital indicate it has economic strengths that could support long-term value creation, making current valuation levels possibly short-lived.

Growth Considerations

While growth metrics present a varied picture with a rating of 5 out of 10, the company shows strong past performance with slowing future forecasts:

- Past Revenue growth averaging 34.59% each year over recent years

- Past EPS growth averaging 42.10% in spite of a small recent drop of 4.77%

- Anticipated future Revenue growth of 5.10% each year

- Expected EPS growth of 4.19% going forward

The shift from outstanding past growth to more measured future forecasts might partly clarify the discounted valuation. For value investors, this makes a possible opening if the market has overreacted to the growth slowdown while ignoring the company’s maintained profitability and financial soundness.

Investment Implications

The mix of discounted valuation, high profitability, and good financial health offers a thought-provoking case for value-focused investors. The company’s current valuation multiples seem to account for the growth slowdown while possibly undervaluing the persistence of its profitability and cash flow generation. The large discounts to industry peers across several valuation metrics, combined with top-level profitability and sound financial health, indicate the stock may provide favorable risk-reward features for investors willing to wait for the valuation difference to narrow.

For investors curious about similar chances, our Decent Value Stocks screen frequently finds companies with appealing valuations and good fundamentals. Readers can view the full fundamental analysis report for Lantheus Holdings for a more detailed look at the metrics covered.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions. Past performance does not guarantee future results, and all investments carry risk including potential loss of principal.