Alphabet Stock Off Its Peak – Is It Undervalued? It Could Be If FCF Stays Strong

Image by Markus Mainka via Shutterstock.jpg)

Markus Mainka via Shutterstock

Alphabet Inc. (GOOG, GOOGL) stock has declined from its recent peak. But is there any significant upside from here? It’s possible, especially if its next 12 months’ free cash flow (FCF) remains strong. It could be up to 25% too cheap.

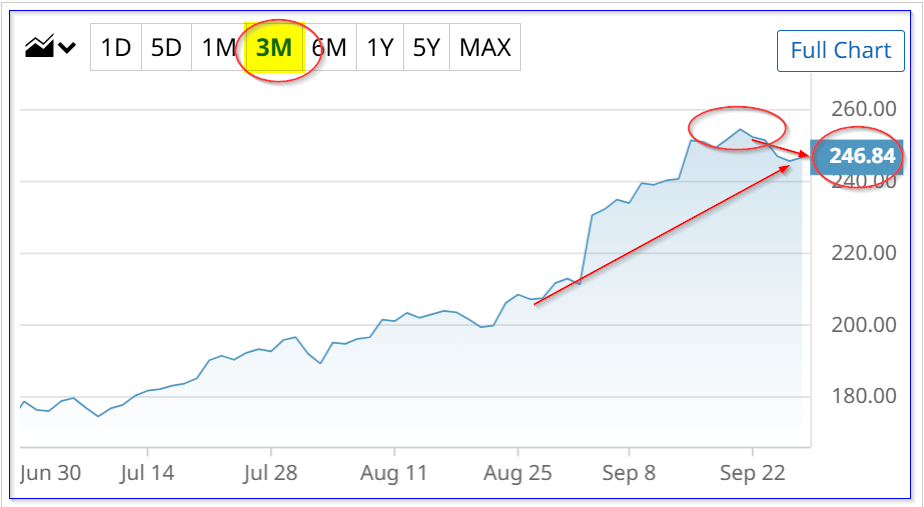

GOOGL is at $246.61 in midday trading on Friday, Sept. 26. This is down from $254.72 on Sept. 19. This article will show why GOOGL could be worth between +12% and +25% more at $309 per share over the next year.

(Click on image to enlarge)

GOOGL stock – last 3 months – Barchart – Sept. 26, 2025

The idea here is that if Alphabet can produce a strong FCF margin over the next several quarters, the stock could move significantly higher. Let’s look at this.

Historical P/E Valuation

I discussed a target price for Alphabet in my last Barchart article three weeks ago on Sept. 3: “Large Unusual Options Activity in Alphabet Options Shows the Stock Is Undervalued.”

Based on its historical price-to-earnings (P/E) multiple, I argued that its historical trailing P/E has been 25 to 26 times.

For example, Seeking Alpha shows that the historical 5-year P/E has been 25.61x, and Morningstar reports that it’s been 24.67x. So, let’s use a 25.14x historical multiple.

Now, Seeking Alpha shows that earnings per share (EPS) this year are expected to be $9.94 and next year $10.67. So, its next-12-month (NTM) estimate is $10.31 per share:

$10.31 EPS NTM x 25.14 = $259.19 per share target

And, by the end of 2026, we could expect GOOGL stock to be at $268.24:

$10.67 x 25.14 = $268.24 target

That is 8.77% higher than today’s price.

However, Alphabet’s stock could be worth much more based on free cash flow (FCF) expectations.

Valuation Based on Free Cash Flow

Another way to look at Alphabet is to simply assume that, despite its lower Q2 free cash flow (FCF) margins, it will continue to make strong year-over-year (Y/Y) or trailing-12-month (TTM) margins.

I discussed Alphabet’s lower FCF margins in a July 27 Barchart article (“Alphabet Posts Lower Free Cash Flow and FCF Margins – Is GOOGL Stock Overvalued?“).

For example, the Q2 FCF margin was just 5.5% and the TTM margin was 18.0%.

But, since then, there are indications that its underlying business will stay intact and the company’s AI initiative will pay off.

After all, in 2024, it made a 20.79% FCF margin, according to Stock Analysis. And it was higher in Q1 at 20.82%, again on a TTM basis.

So, it’s not unreasonable to assume that Alphabet could average at least a 20% FCF margin over the next 12 months (NTM).

For example, analysts now expect revenue this year will be about $395 billion and next year $440.3 billion. That works out to an NTM forecast of $417.65 billion:

$417.65 billion NTM revenue x 0.20 FCF margin = $83.53 billion FCF

That would be 25% higher than the $66.728 billion in TTM FCF as of Q2. That could potentially imply a higher stock price. Here’s why.

Alphabet’s market cap today is about $2.989 trillion. That implies that its FCF yield is 2.2%:

$66.728b TTM FCF / $2,989 b = 0.0223 = 2.23% FCF yield

Therefore, let’s assume the market will give Alphabet a 2.23% yield when it produces higher FCF over the next 12 months:

$83.53b / 0.0223 = $3,745.7 billion market cap

That is +25.3% higher than today’s market cap. In other words, GOOGL stock could be worth 25% more:

$246.61 x 1.253 = $309 per share

Summary Valuation

Yahoo! Finance reports an average of $236.82, which is lower than today’s price, but AnaChart’s survey shows a price target of $269.23. That provides an average survey target of $253, slightly higher than today’s price.

Nevertheless, the Yahoo! Finance target price is higher than the $221.25 price target just three weeks ago, as seen in my prior Barchart article.

The bottom line here is that, based on these three methods, GOOGL is still cheap:

P/E valuation …….. $268.24

FCF valuation ………$309.00

Analysts ………………$253.00

Average Target ….. $276.75

That is 12% higher than today’s price. The point here is that Alphabet still looks undervalued, anywhere from 12% to 25% too cheap.

One way to play this is to sell short out-of-the-money (OTM) put options.

Shorting OTM Puts

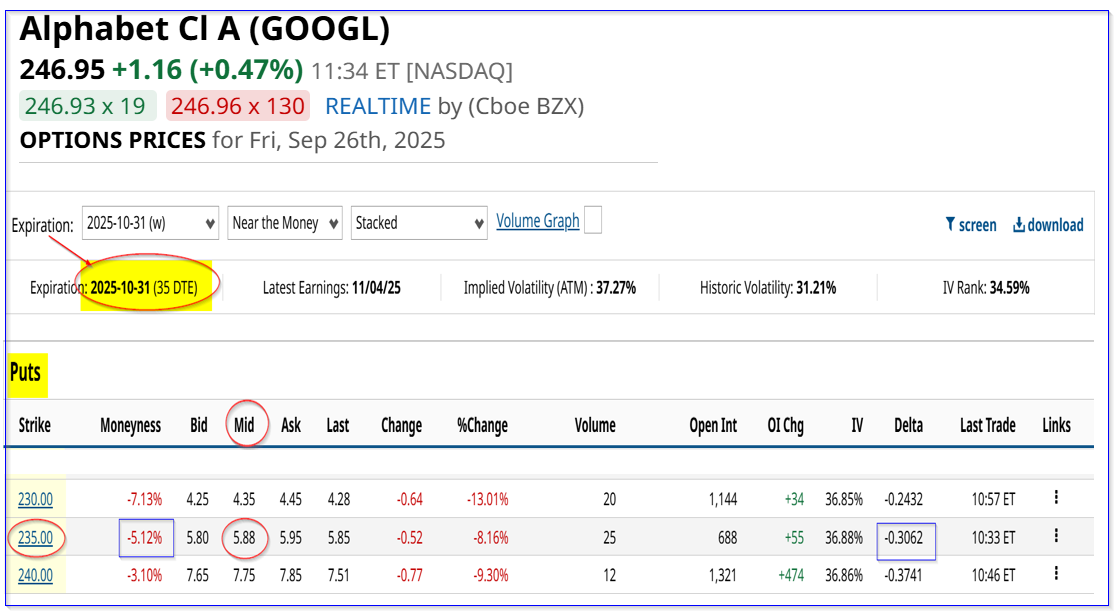

For example, the Oct. 31, 2025, expiry period shows that the $235.00 put option, which is less than 5% below today’s price, has a midpoint premium of $5.88.

That means that a short-seller of these put options can make an immediate yield of 2.50% (i.e., $5.88/ $235.00).

(Click on image to enlarge)

GOOGL puts expiring Oct. 31, 2025 – Barchart – As of Sept. 26, 2025

This also sets a lower potential buy-in point for a short-seller (if GOOGL falls to $235.00 on or before Oct. 31):

$235.00 – $5.88 = $229.12

That is about 7% below today’s price. So, it provides good downside protection against a potential unrealized loss (i.e., if GOOGL falls to $235.00).

Moreover, if this play is repeated over the next 6 months, the investor stands to make an expected return (ER) of +15% (i.e., 2.5% x 6). That is almost as good as buying and holding GOOGL stock, as seen by the valuation estimates above.

The bottom line is that an investor can make a good yield shorting OTM GOOGL puts and set a lower buy-in point. It also allows existing shareholders to potentially lower their average cost as well as collect extra income.

Moreover, the potential upside, assuming a $309 target, is almost +35% (i.e., $309.00 / $229.12 = 1.3486 -1 = +34.86%).

The bottom line is GOOGL stock looks cheap here and shorting OTM puts is a good way to play this.

More By This Author:

Intel Stock Soars Along With Unusual Put Options Activity – Is INTC Stock Overvalued?

Palantir Stock Could Still Be 20% Undervalued As Analysts Raise Their Forecasts

Nvidia Stock Is Slowly Moving Higher – Short Put Plays Could Work Here