Marsh & McLennan Cos (NYSE:MMC) Identified by Caviar Cruise Investment Screen for Strong Financials

Professional services firm Marsh & McLennan Cos (NYSE:MMC) has been identified by the Caviar Cruise investment screen, a systematic process intended to find companies with lasting competitive strengths and sound financial features. This approach focuses on long-term ownership of businesses showing steady revenue increases, growing profitability, high capital allocation effectiveness, and good financial condition. The method favors measurable data that indicate operational quality and financial strength, making it especially useful for investors looking to establish holdings in companies able to increase value over long timeframes.

Financial Performance and Growth Data

The Caviar Cruise screen demands companies show both revenue and EBIT increases of more than 5% per year over five years, with EBIT growth preferably higher than revenue growth, a sign of better operational effectiveness and possible pricing strength. Marsh & McLennan easily meets these levels, showing the company’s capacity to not only increase its revenue but also turn that growth into greater profits.

- Revenue Growth (5Y CAGR): 6.03% – Above the 5% minimum level

- EBIT Growth (5Y CAGR): 15.58% – Well above both the 5% requirement and revenue growth

- Profit Margin Expansion: Operating margin of 25.39% is better than 91% of industry competitors

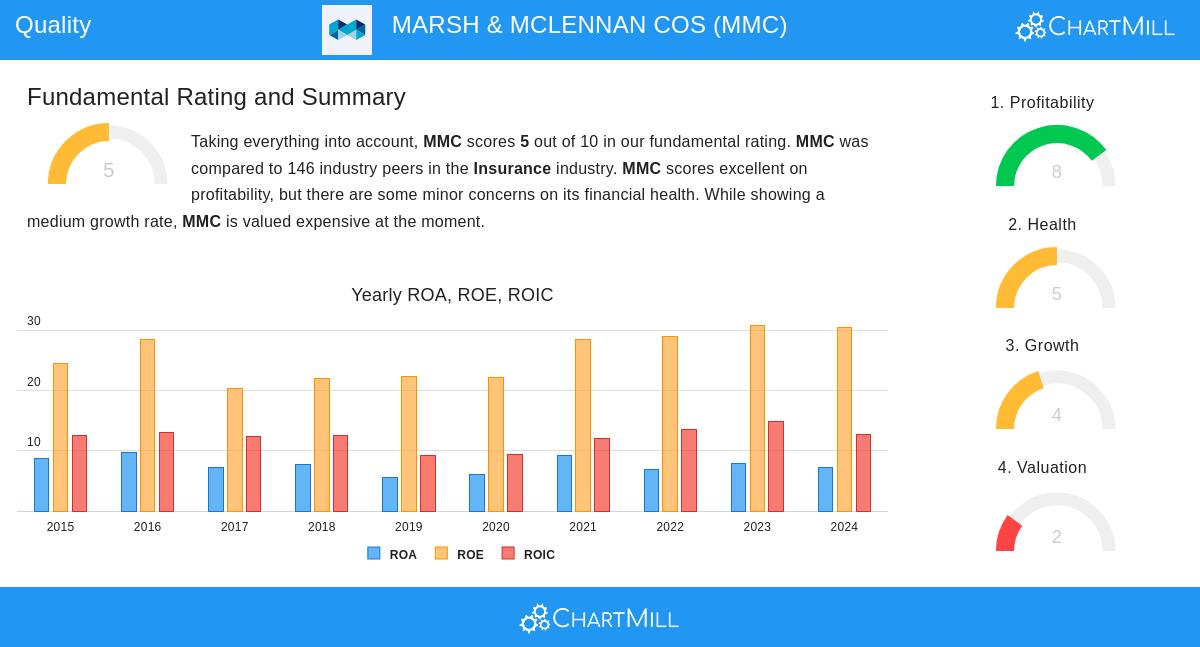

The large difference between EBIT growth and revenue growth shows Marsh & McLennan has effectively used its size to raise profitability, possibly through operational improvements or positive pricing conditions in its risk and insurance services divisions.

Capital Allocation Effectiveness

A fundamental part of quality investing, return on invested capital assesses how well a company produces profits from its capital foundation. The Caviar Cruise method specifically highlights ROIC without cash, goodwill, and intangibles to concentrate on central operational effectiveness. Marsh & McLennan’s results in this area are notable.

- ROIC (Excluding Cash, Goodwill & Intangibles): 55.24% – Much higher than the 15% minimum requirement

- Industry Comparison: ROIC of 12.56% is still better than 98% of insurance industry competitors

This impressive ROIC number indicates Marsh & McLennan needs relatively small capital to sustain and expand its professional services activities, generating substantial value for shareholders through effective capital use.

Financial Condition and Cash Flow Strength

The screen assesses financial stability using debt coverage ratios and profit quality, the transformation of accounting profits into real cash flow. These data points help find companies with maintainable financial frameworks and dependable earnings strength.

- Debt-to-Free Cash Flow: 4.24 years – Inside the acceptable 0-5 year span

- Profit Quality (5-Year Average): 109.53% – Above the 75% level

The company’s capacity to change over 100% of net income into free cash flow shows good earnings strength and allows options for strategic projects, including possible purchases, share buybacks, or dividend growth.

Fundamental Analysis Summary

According to the detailed fundamental analysis, Marsh & McLennan gets a varied but mostly good evaluation. The company is strong in profitability data, scoring 8 out of 10, with outstanding returns on equity and assets that place in the top group of the insurance industry. However, valuation stays a worry with a score of 2 out of 10, as the company sells at higher levels than industry averages on several data points including P/E and enterprise value to EBITDA ratios. Financial condition receives a middle 5 out of 10, with some debt-related worries balanced by sufficient liquidity measures.

Investment Points for Quality Investors

While Marsh & McLennan shows many features wanted by quality investors, several elements need thought. The company’s high valuation may cause hesitation for value-focused investors, although this could be reasonable given its better profitability and market standing. The debt-to-equity ratio of 1.21 shows greater leverage than some cautious investors might like, though the workable debt-to-FCF ratio indicates the company can handle this debt without difficulty.

The company’s business model, providing necessary risk management and consulting services, displays features quality investors usually want: recession durability, pricing strength, and connection with long-term movements toward professional risk management. Its global presence and varied service offerings across Marsh (insurance brokerage), Guy Carpenter (reinsurance), Mercer (consulting), and Oliver Wyman (strategy) give extra steadiness.

For investors wanting to examine other companies that satisfy the Caviar Cruise requirements, the complete screen results give more investment options that share these quality features.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions.