Why I’m Reconsidering Starbucks’ Role in My Portfolio — Is There a Better Investment for Income and Growth?

After five years of holding, I’m way behind where I thought I’d be.

In June 2020, I happily invested in one of my favorite consumer brands: Coffee giant Starbucks (SBUX -0.36%). But after it’s underperformed the returns from the S&P 500 by a wide margin over these five years, it’s high time I reconsidered its role in my portfolio.

I believed that Starbucks stock would provide my portfolio with a blend of growth and income. For growth, I was quite optimistic that the company’s business in China would quickly rebound from the pandemic and unlock much higher earnings. That hasn’t happened. With it now looking for strategic options for its China business, it’s time for me to wave the white flag here.

https://www.youtube.com/watch?v=56Ci0TjoOq0

Regarding income, Starbucks didn’t disappoint. It’s increased its dividend payment every year that I’ve held it, and is currently on a 14-year streak of doing that. And as of this writing, the dividend yield is approaching 3%, which is close to the highest it’s ever been.

Therefore, I can’t really complain when it comes to dividend income from Starbucks stock. But growth has been lacking. Going back to just before the pandemic started, Starbucks has averaged a single-digit compound annual growth rate (CAGR) for revenue. This often isn’t good enough to propel market-beating stock performance. So the question is: Can I find a comparable dividend-paying stock that offers better growth? Indeed, there are some options.

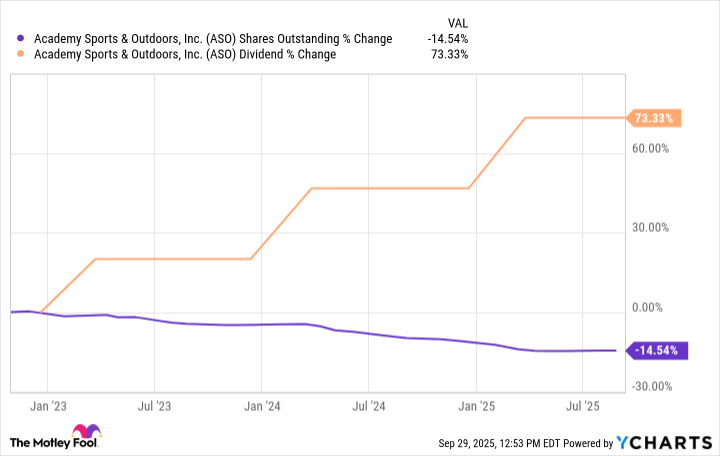

1. Academy Sports & Outdoors

With only 300 locations, sporting goods retailer Academy Sports (ASO 1.77%) is easy to overlook. But if management has its way, the company could put up better top-line growth than Starbucks from here.

Perhaps the biggest way that Academy Sports is driving revenue growth is by opening new stores. This year, it hopes to open up to 25 locations. It had already opened eight of these by the end of the second quarter of 2025. Past guidance suggests that the company intends to open around 150 additional locations by the end of 2028.

These new store openings could allow Academy Sports to deliver a double-digit growth rate in coming years. Management is also known for methodically returning cash to shareholders. It buys back stock, and its quarterly dividend has grown at a nice pace in recent years.

ASO Shares Outstanding data by YCharts.

With a dividend yield of only 1%, Academy Sports won’t necessarily attract income investors today. But those with a long-term view hope to ride the company’s growth plans to much higher earnings in time, which could result in much better dividend income down the road.

2. Arcos Dorados

Restaurant chain Arcos Dorados (ARCO -0.15%) owns the rights to the McDonald’s brand in 21 countries in Latin America and the Caribbean, allowing it to own and operate franchised locations and sub-franchise to other operators. With over 2,400 locations, it’s the largest independent McDonald’s franchisee.

Differences in currency exchange rates are masking double-digit revenue growth for Arcos Dorados. For the second quarter of 2025, the company reported just 3% year-over-year growth. But adjusting for currency fluctuations, it grew by 15%. This includes both same-store sales growth and the contribution of new restaurant locations.

With a 3.5% dividend yield, Arcos Dorados stock is more attractive than Starbucks stock as an income investment. The company also pays out just a small portion of its earnings as a dividend, leaving plenty of room for future growth.

About one-third of Arcos Dorados’ locations are sub-franchised. And like McDonald’s itself, Arcos Dorados generates some revenue from its franchisees via rental income — it owns the land and buildings at nearly 500 locations. This real estate layer to the business can make it a stronger investment compared to other restaurant companies.

3. Stick with Starbucks?

Over my investing career, I’ve learned to only sell a stock after taking plenty of time to think it over. So while I’m thinking about selling Starbucks stock and buying a replacement that’s growing faster and still offers income, it’s not a done deal. In fact, I see some reason to continue holding Starbucks stock.

It’s been just over one year since Starbucks hired new CEO Brian Niccol, and he’s still trying to reinvigorate the brand. That starts with bringing back the more inviting coffeehouse atmosphere. The company just announced that it will close hundreds of locations that don’t fit its vision.

Niccol’s plan comes with an expensive price tag of around $1 billion. But investors’ expectations are now low, and Starbucks can start bouncing back as difficult decisions pay off.

For now, I believe the downside risk for Starbucks stock is low because it’s still a top consumer brand and Niccol has a good reputation as an operator. Academy Sports and Arcos Dorados are on my radar as potentially filling the role in my portfolio currently filled by Starbucks. But I see no reason to rush this decision today, so I’ll keep holding Starbucks stock for now.

Jon Quast has positions in Academy Sports And Outdoors and Starbucks. The Motley Fool has positions in and recommends Starbucks. The Motley Fool recommends Academy Sports And Outdoors. The Motley Fool has a disclosure policy.