STRIDE INC (NYSE:LRN): An Affordable Growth Stock Poised for Continued Expansion

Investors looking for growth chances at fair prices often use screening methods that find companies showing good expansion possibility without high costs. The “Affordable Growth” method focuses on stocks with good growth paths, firm basic business condition, and profit measures, all while keeping fair prices. This system tries to identify companies set for ongoing expansion but selling at prices that do not completely show their future possibility, possibly presenting interesting risk-reward situations for long-term investors.

Growth Path

STRIDE INC (NYSE:LRN) shows interesting growth features that build the base of its attraction as an affordable growth choice. The company’s past results display notable expansion, while future signs point to continued speed.

- Earnings Per Share has jumped 28.91% over the last year, with a typical yearly growth rate of 58.07% over recent years

- Revenue grew 17.90% in the last year, keeping an 18.24% typical yearly growth path

- Future EPS growth is estimated at 22.40% each year, supported by expected revenue growth of 9.06%

These growth measures are much higher than industry standards and supply the needed expansion part for affordable growth investing. The mix of good past results and large future growth hopes builds an interesting story for investors looking for companies in their growth stage.

Valuation Check

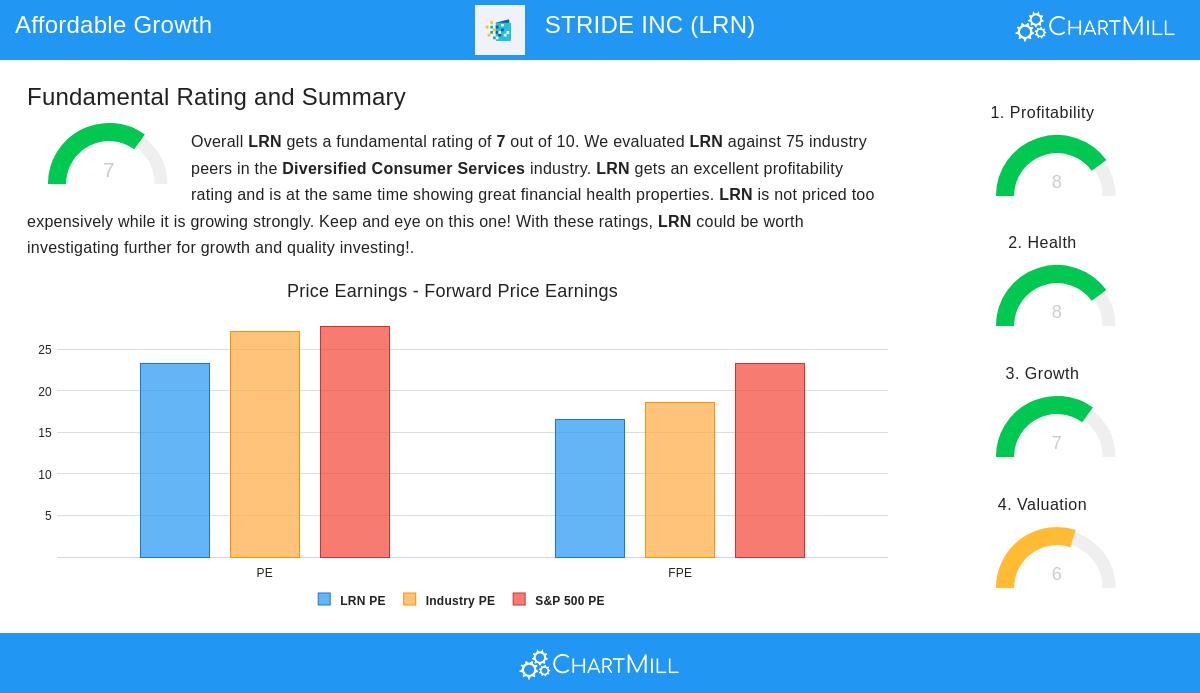

The valuation view for Stride shows a notable situation where standard measures display fair pricing compared to both industry friends and wider market guides. While some simple numbers might seem high, comparison study shows interesting placement within its field.

- P/E ratio of 23.26 looks good against the industry average of 27.16 and S&P 500’s 27.76

- Forward P/E of 16.58 is lower than the S&P 500’s 23.21 and seems interesting compared to industry friends

- Enterprise Value to EBITDA ratio places Stride less expensive than 73.33% of industry rivals

- Price/Free Cash Flow ratio is better than 78.67% of industry friends

The PEG ratio, which changes the P/E for growth hopes, points to especially interesting valuation when thinking about the company’s growth path. This mix of fair simple valuation and good relative value compared to friends makes Stride notable as a possibly underappreciated growth story.

Profit and Money Condition

Beyond growth and valuation, Stride shows very good operational effectiveness and money stability that back its lasting expansion story. The company’s profit measures display good performance, while its balance sheet gives enough support for continued spending.

Profit highlights include Return on Invested Capital of 15.98%, doing better than 93.33% of industry friends, and Return on Equity of 19.46%, beating 85.33% of rivals. The company keeps a sound Profit Margin of 11.97% and Operating Margin of 17.44%, both showing upward moves in recent years. Money condition signs show a firm balance sheet with a Current Ratio of 5.39 and Quick Ratio of 5.27, both much higher than industry averages. The Altman-Z score of 7.36 shows very low failure risk, while controllable debt levels with a Debt to Equity ratio of 0.31 give money flexibility.

These good profit and condition measures are important for affordable growth investing as they lower basic risks while supporting the company’s ability to pay for future expansion from inside. The mix of very good returns on capital, growing margins, and careful money management creates a base for lasting growth without heavy dependence on outside money.

Investment Points

Stride’s full basic profile, explained in the full basic study report, presents an interesting case for growth-focused investors looking for fair prices. The company works in the education technology field, giving K-12 education and career learning services through technology-based platforms. This placement in a steadily growing market matches its good operational measures.

The company’s balanced picture, mixing above-average growth with fair valuation and very good money condition, fits well with the affordable growth idea. While future growth rates are thought to slow from unusual past levels, they stay much higher than industry standards and are backed by good profit and a clear balance sheet.

For investors wanting to find similar chances, more affordable growth choices can be seen through our custom stock screener that finds companies with good growth, fair prices, and firm basic features.

Disclaimer: This study is based on basic data and ratings given by ChartMill.com and shows a neutral check of the company’s money measures. This information is for learning and study purposes only and should not be seen as investment guidance or suggestions. Investors should do their own study and talk with money advisors before making investment choices. Past results do not promise future results, and all investments have risk including possible loss of original money.